{kind=link}

Well, budgeting is just being intentional. your money. It’s telling your money where to go in for a lot of Americans. You know, we filed taxes than we think back. To 2024. And thank Made all this money. But where did it go? And so I don’t want that to happen to you this year.

So regardless of where you are having a budget is so so important, is it still possible to budget when you’re deep in debt? It is. And you want to put your debt and your budget’s most effective way to budget of the 0 based budgets are going to take your income for the month.

Prices are high, rent is wild, and paychecks feel like they vanish in days. If you are asking yourself how to budget salary in USA 2025 or how to budget 60k a year in a clear way, you are not alone.

Key take aways

- What your real take-home pay looks like in 2025

- How to split your income using a simple rule

- Budget examples for $40k, $50k, $60k, and $70k salaries

- Cost-of-living examples for major U.S. cities

- Smart money habits that actually work

How to Budget Your Salary in USA (2025)

Let us start with a quick roadmap before we go deeper into the details.

If you want a simple answer to how to budget salary in USA 2025, here is the high-level process:

- Figure out your real monthly take-home pay, not just your salary.

- List your true needs first, like rent and food.

- Decide how much goes to wants, savings, and extra debt.

- Use a simple rule of thumb, like 50/30/20, as your starting point.

- Track, tweak, and repeat every month.

Once you have this flow, learning how to budget 60k a year becomes a lot less stressful.

Step 1: Know your real take-home pay after taxes

Your gross pay is what your employer says you make, like $60,000 a year. Your net pay (or take-home pay) is what actually lands in your bank account after federal taxes, state taxes, Social Security, and Medicare.

Example: $60,000 salary in 2025 (average U.S. estimate)

| Income Type | Amount |

|---|---|

| Yearly Gross | $60,000 |

| Monthly Gross | ~$5,000 |

| Monthly Take-Home (After taxes, SS + Medicare) | ~$3,700–$3,900 |

That is a big gap. If you build a budget from the $1,000+ number, things will never line up. Grab your latest pay stub and write down the average monthly net pay. That is the number your budget should use.

Step 2: List your true monthly needs first

Needs keep the lights on and the roof over your head. In plain terms, needs are:

- Housing (rent or mortgage)

- Basic groceries

- Utilities and internet

- Transportation (gas, transit, car insurance, basic repairs)

- Health insurance and key medical costs

- Minimum debt payments

Write down every fixed bill, like rent, phone, and insurance. Then look at variable bills, like power or gas, and use a 3‑month average.

Needs come first because if they are not covered, nothing else works. Wants and extra debt payments come after these basics.

Read More: 20 Frugal Living Tips: Enjoy Life with Less Spending

Step 3: Set limits for wants, savings, and debt payoff

Once needs are covered on paper, the rest of your take-home pay can go to:

- Wants: eating out, streaming, hobbies, shopping, travel, nicer upgrades.

- Savings: emergency fund, house down payment, retirement, big future goals.

- Extra debt payoff: more than the minimum on credit cards, student loans, or personal loans.

The key word here is limit. Without a cap on wants, food delivery and random online orders eat your budget alive.

Even if you start with 5 to 10 percent of your take-home pay going to savings, that is fine. Tiny, steady moves toward a 3 to 6 month emergency fund or retirement are much better than waiting for “extra” money that never appears.

If you want a deeper breakdown of savings strategy, check this guide: 🔗 How Many Savings Accounts Can I Have?

Let’s make your 2025 salary go further starting today.

Here is one paycheck routine video that fits well with what you are about to read:

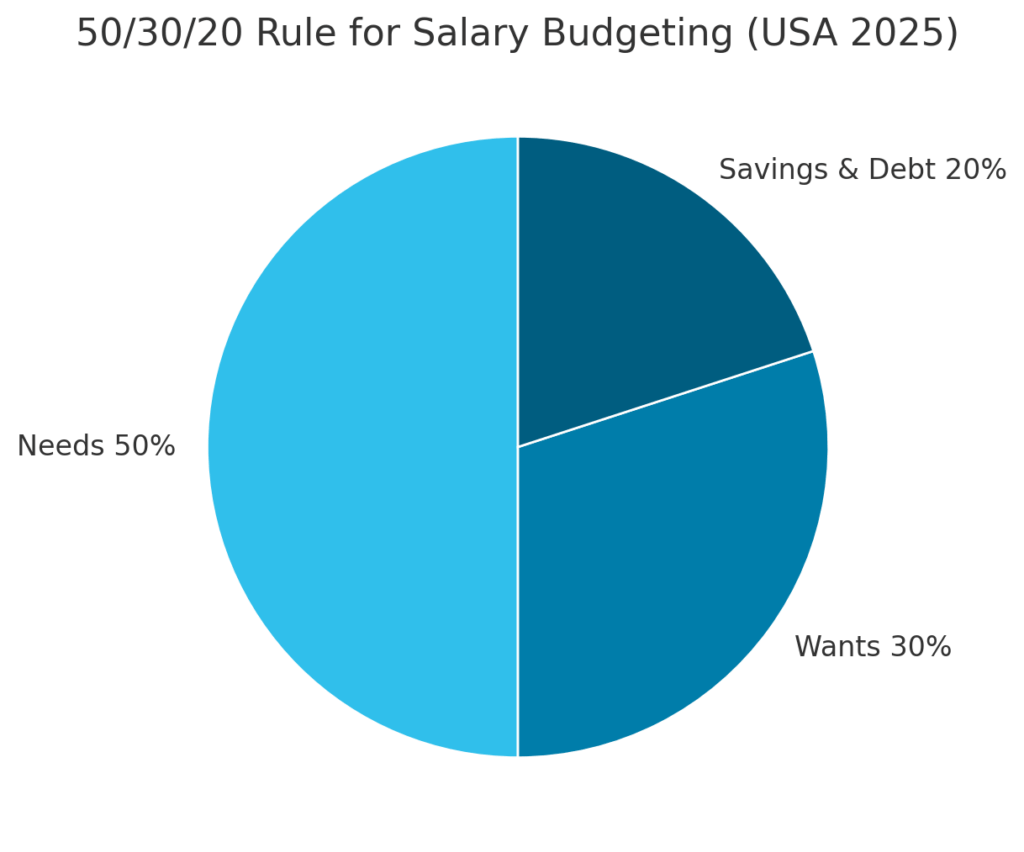

The 50/30/20 Rule — Best Starter Plan for Salary Budgeting

If you love clean frameworks, the 50/30/20 rule is a simple, flexible way to answer how to budget 60k a year.

This classic rule helps you split your take-home pay:

| Category | % of Net Income | Purpose |

|---|---|---|

| Needs | 50% | Essentials |

| Wants | 30% | Lifestyle choices |

| Savings + Debt Payoff | 20% | Financial growth |

You can play with the exact percentages, but this is a strong starting point for many people on a $60,000 income. more details you can read this article 50/30/20 Rule: How It Works

How the 50/30/20 rule works for a $60,000 yearly income

Let us use a simple case. Say your $60,000 salary in 2025 gives you about $3,800 per month after taxes.

Using 50/30/20:

| Category | Amount | Notes |

|---|---|---|

| Needs (50%) | ~$1,900 | Housing, groceries, insurance |

| Wants (30%) | ~$1,140 | Eating out, hobbies, streaming |

| Savings + Debt (20%) | ~$760 | Emergency fund, investing |

That is it. Now your entire month fits in three main buckets. Anytime money leaves your account, you can ask, “Is this a need, want, or savings/debt?” That quick question keeps your plan on track.

A breakdown from Yahoo Finance that shows what an ideal $60,000 salary budget looks like lines up closely with this kind of split, which is one reason so many planners use it.

Sample monthly budget on a $60k salary in 2025

Here is one simple sample budget for a single person in an average‑cost city on a $3,800 monthly take-home:

| Category | Example amount |

|---|---|

| Rent | $1,300 |

| Utilities & internet | $200 |

| Groceries | $350 |

| Transportation & gas | $250 |

| Insurance (health, auto) | $200 |

| Minimum debt payments | $150 |

| Total needs | $2,450 |

| Eating out & coffee | $250 |

| Streaming & subscriptions | $60 |

| Shopping & hobbies | $250 |

| Travel & fun | $150 |

| Total wants | $710 |

| Emergency fund savings | $300 |

| Retirement or investments | $250 |

| Extra debt payoff | $90 |

| Short‑term savings goals | $100 |

| Total savings/debt | $740 |

Total: $2,450 + $710 + $740 = $3,900, a touch over our $3,800 example. In real life, you would trim one or two lines to bring it back in range.

If you live in a high‑cost city, rent might be closer to $1,700 or more each month, like in many 2025 estimates. In that case, you slide numbers around, but the structure stays the same.

When you should adjust the 50/30/20 rule for your life

Real life rarely fits neat formulas. Some people on a $60k income do better with a 60/20/20 or 60/25/15 split, especially if:

- Rent eats a bigger slice of your budget.

- You have heavy student loans.

- You are saving hard for a house or early retirement.

The 60/20/20 rule breakdown on Nasdaq is a good example of how people bend the classic rule when needs take more than half of their take-home pay.

Think of 50/30/20 as a starting grid, not a strict rule. The real win is steady progress: bills paid, debt shrinking, savings growing.

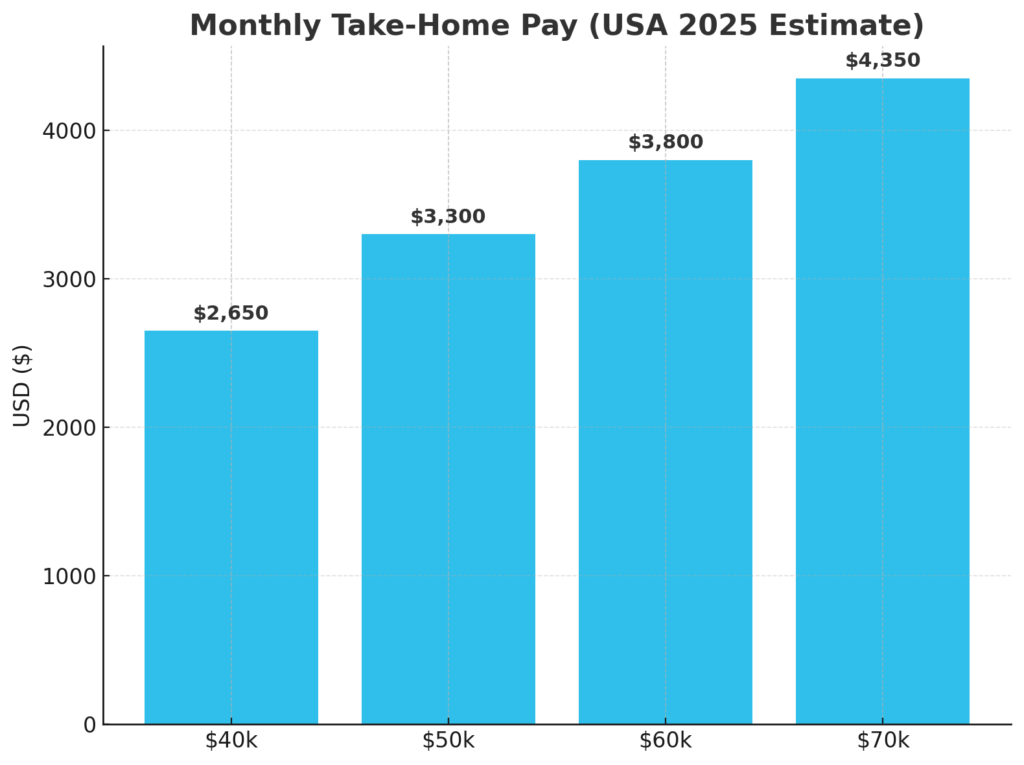

Budget Examples for Different Salaries (2025)

| Gross Salary | Monthly Take-Home | Suggested Split |

|---|---|---|

| $40,000 | ~$2,650 | 60/20/20 |

| $50,000 | ~$3,300 | 55/25/20 |

| $60,000 | ~$3,800 | 50/30/20 |

| $70,000 | ~$4,350 | 45/30/25 |

Try plugging your own numbers into this download: ➡ SmartInvestIQ Budget Template (Free)

Simple budgeting habits to make your 2025 salary go further

The structure is great, but habits make the math real. These small routines help your budget work in the background while you live your life.

Track every dollar with apps or a simple spreadsheet

Tracking is the base of any strong budget. If you do not know where the money went, you cannot fix anything.

You can:

- Use a simple spreadsheet with columns for date, store, category, and amount.

- Use a basic budgeting app that connects to your bank and tags spending.

- Do a weekly “money check‑in” so nothing piles up.

Most people find that one month of honest tracking gives enough data to tighten categories and spot leaks.

Automate savings and bill payments so your budget runs itself

Automation turns good intentions into real results. A few ideas:

- Set an automatic transfer from checking to savings the day after each paycheck.

- Use direct deposit splits if your employer offers them, so part of your pay goes straight to savings or investments.

- Put major bills like rent, utilities, and minimum debt payments on auto‑pay.

This is the “pay yourself first” idea in action. You build savings even on a $60k income without relying on daily willpower.

Cut quiet money leaks and upgrade your budget over time

Every budget has quiet leaks that drain cash:

- Subscriptions you forgot about.

- High bank fees or credit card fees.

- Food delivery that sneaks in three times a week.

- Driver‑through habits when you already bought groceries.

Go line by line through your last month of spending. Cancel or cut what no longer matches your priorities. Many people free up $50 to $200 per month this way, and that money can go to extra debt payoff or faster savings.

Every few months, run a short review:

- Has your rent, income, or insurance changed?

- Are you closer to your savings goals?

- Do your 50/30/20 (or 60/25/15) numbers still feel right?

Small upgrades beat huge, short‑term “money detox” plans. Over a year, those tweaks can reshape your whole financial picture.

Conclusion

In the USA in 2025, learning how to budget salary in usa 2025, how to budget 60k a year comes down to a clear plan, not perfect math. When you know your real take-home pay, give every dollar a job, and use a simple rule like 50/30/20, a $60,000 income starts to feel more under control.

You do not have to change everything at once. Pick one habit from this guide, build a first draft budget for next month, and test it. Then adjust, improve, and keep going.

Your future self will be very glad you started today.