{kind=link}

Table of Contents

Did you know that your credit score could be costing you hundreds of dollars extra on your car insurance? Although it my seem unfair but in most states, insurance companies use your credit history as major factor to determine your premium. The reason most insurance companies use your credit history is the system because system is designed to keep charging you more when you can least afford it.

But the good news is you can take control of this situation and potentially save significant money by understanding how credit and insurance expenses are related.

In this guide we will explain how does credit score affect Car Insurance rates and discover practical steps to improve your score and lower your premiums in the process.

Why Insurers Use Your Credit Score to Set Rates

When insurance companies set your rates, they’re trying to assess the risk of you filing a claim. Studies have consistently found that drivers with lower credit scores are more likely to file claims than those with higher credit scores.se with higher scores.

Here are the key facts behind this widely debated practice:

- The financial impact is real: Low-credit drivers frequently pay 40–50% more for auto insurance than drivers with good credit, which can total up to $500–1,500 more annually.

- It’s legal almost everywhere: 47 states allow insurance companies to factor in your credit-based insurance score when setting rates. So far, just California, Hawaii, and Massachusetts have made this practice illegal.

- Even safe drivers aren’t exempt: Your spotless driving record won’t always help if your credit score is poor. In many cases, drivers with bad credit end up paying more than those with accidents or tickets, as long as those drivers have excellent credit.

The fact that most insurance companies don’t want you to realize is that your credit score frequently has a greater influence on your insurance prices than little infractions or accidents. Improving your credit can be the quickest way to save money if you’re having trouble paying hefty rates!

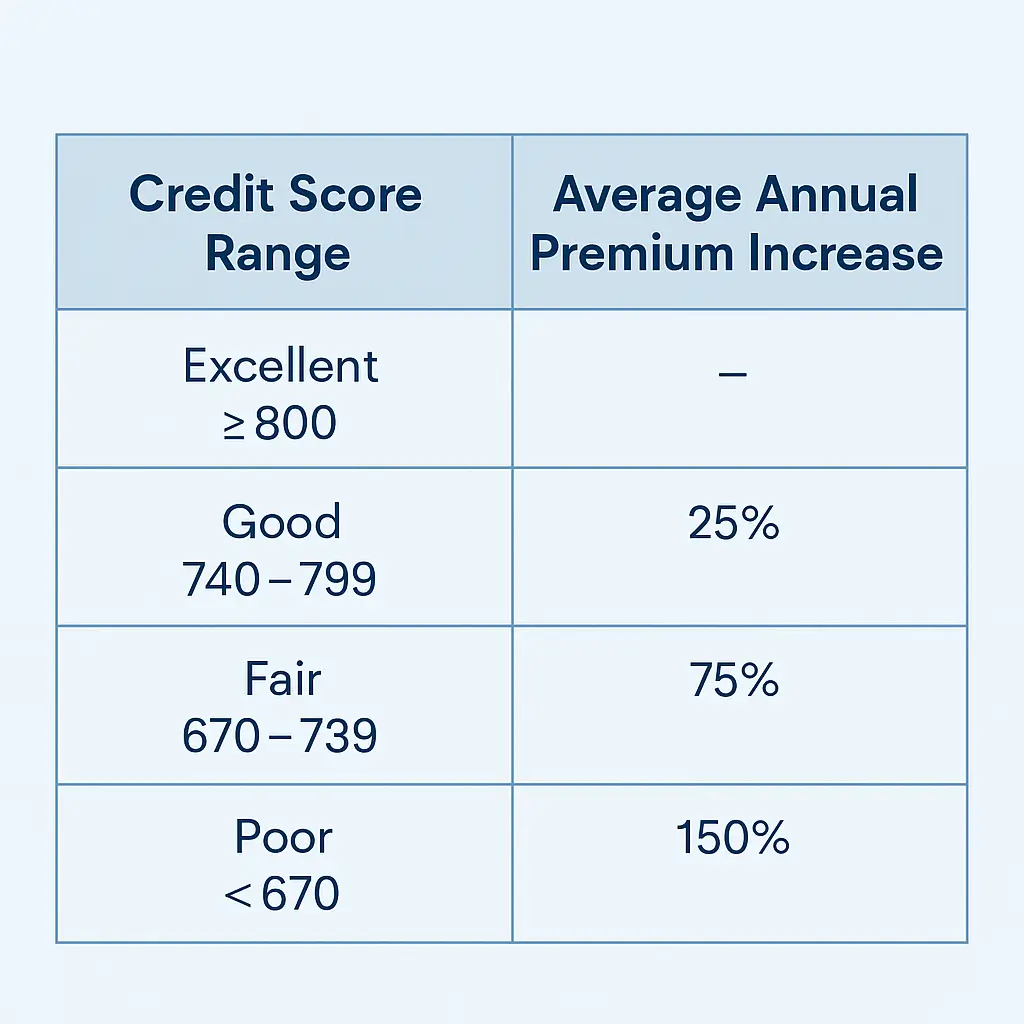

How Much Does a Low Credit Score Raise Your Insurance Costs?

This implies that, even with the same driving history, car, and other details, a driver with bad credit may pay more than twice as much for the same coverage as a driver with good credit.

Why Do Insurance Companies Use Credit Scores Anyway?

A credit-based insurance score is different from your traditional FICO or VantageScore. It evaluates:

- Payment timeliness

- Credit utilization

- Total debt

- Length of credit history

- Types of credit

- New credit inquiries

These factors create a profile insurers use to determine how risky you are as a customer—not financially, but from an insurance standpoint.

Signs Your Credit Is Costing You More on Car Insurance

The financial impact can be dramatic. A driver with excellent credit may pay up to 50% less than someone with poor credit, even with the same driving record.

For example:

- Excellent Credit: $850/year

- Average Credit: $1,200/year

- Poor Credit: $1,700–$2,000/year

This variation shows how your credit standing can shape your financial obligations beyond loans or credit cards.

5 Proven Ways to Improve Your Credit Score (And Lower Your Insurance Rates)

1. Pay Bills on Time

On-time payments are one of the most important parts of your credit profile. Even a single late payment can damage your score and remain visible on your credit report for up to seven years, making it harder to qualify for loans or get favorable interest rates.

2. Lower Credit Card Balances

Make an effort t0 keep your credit card balances well below your total credit limit. Using less than 30% is recommended, but staying under 10% can lead to even better results. Keeping your balances low shows lenders that you manage credit responsibly and can help improve your credit score over time.

3. Don’t Open Too Many New Accounts

Every new credit application results in a hard inquiry, which can lower your score. Too many inquiries in a short time may signal financial instability.

4. Keep Long-Term Accounts Open

Older accounts contribute to your credit history length. Closing them can shorten your average account age and hurt your score.

5. Review and Dispute Credit Report Errors

You have the right to request a free credit report once a year from each of the major credit bureaus (Experian, Equifax, and TransUnion) at AnnualCreditReport.com. Check for mistakes like duplicate accounts, outdated information, or fraudulent activity and file disputes to correct them.

Shop Around for Better Insurance Rates

Not all insurers weigh credit the same. One company might penalize a lower score heavily, while another might not. Compare quotes across at least three to five providers, especially if your score is average or improving.

Look for companies that:

- Offer usage-based programs

- Provide loyalty or bundling discounts

- Allow for re-evaluation after credit improvement

Frequently Asked Questions (FAQs)

1. How does credit score affect car insurance rates?

Car insurance companies use credit-based scores to assess risk. A lower score signals a higher likelihood of filing a claim, which results in higher premiums. Conversely, a higher score can earn you better rates and discounts.

2. Do all states allow insurers to use credit scores?

No. States like California, Hawaii, and Massachusetts prohibit the use of credit in setting car insurance rates. In most other states, however, it’s legal and widely used.

3. Can improving my credit score lower my current insurance rate?

Yes. Some insurers allow mid-term reviews of your score. If you’ve significantly improved it, contact your insurer to request a premium reevaluation.

4. Is it legal for insurers to use credit scores?

Yes, in most states. The use of credit-based insurance scores is regulated, and insurers are required to follow strict rules to ensure fair use.

5. What’s the difference between a credit score and a credit-based insurance score?

While both use similar credit information, a credit score estimates how likely you are to repay a loan, whereas a credit-based insurance score assesses the likelihood of you filing insurance claims.

Final Thoughts

You might be surprised to learn how much your credit score affects your entire financial situation, including the cost of your auto insurance. In addition to lowering prices, having a high credit score opens up possibilities for insurer discounts, simpler renewals, and greater coverage choices.